Nokia Thought It Was Bold Too

There's a version of financial analysis that would look at Amazon right now and panic.

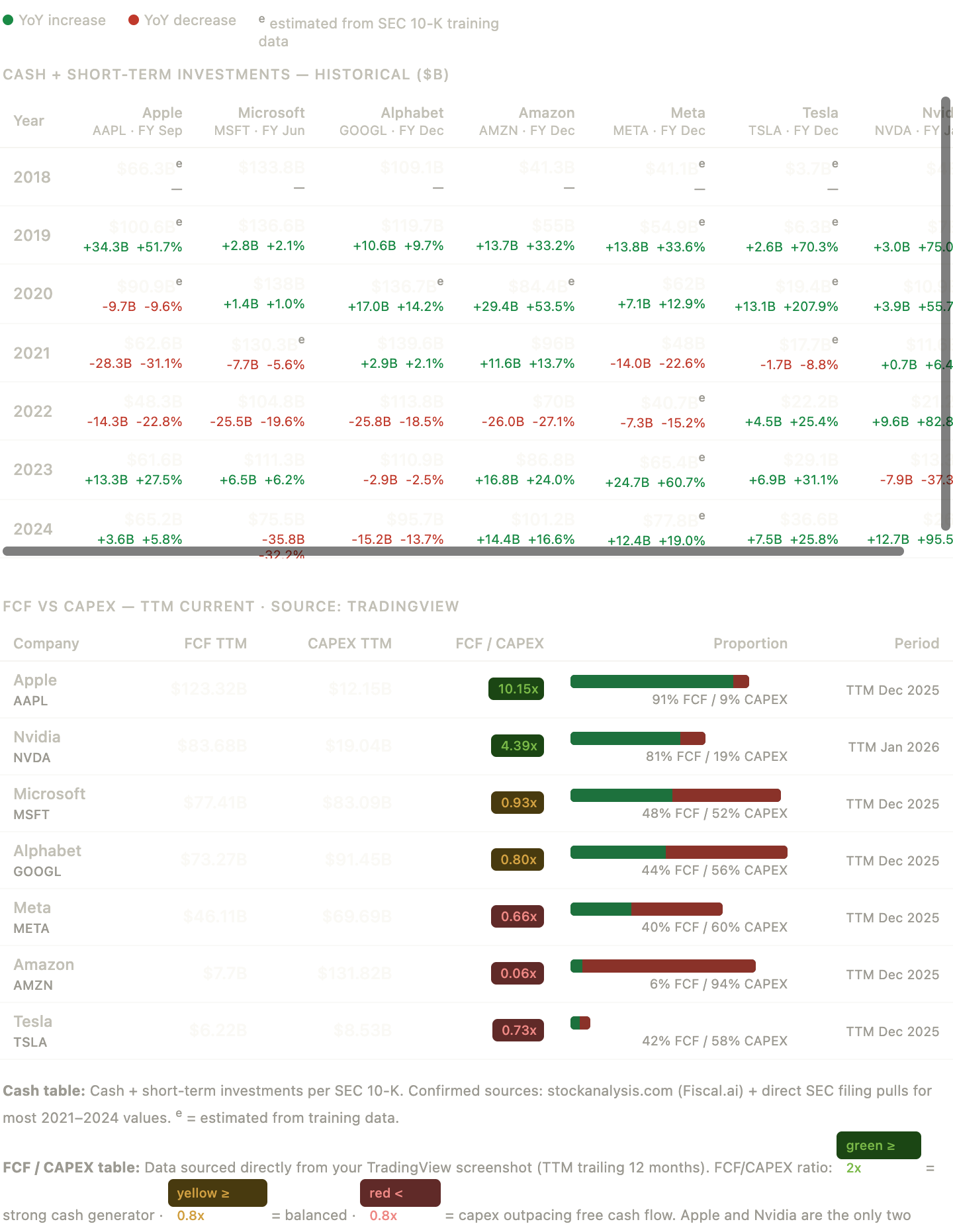

In the last twelve months, Amazon spent $131 billion in capital expenditures. Their free cash flow — the money left over after the business pays its bills and maintains itself — was $7.7 billion. That means for every dollar they generated in free cash flow, they spent seventeen on infrastructure. On paper, that looks like a company running toward a cliff.

It might be. But it also might be the most rational thing any company is doing right now.

The difference between those two outcomes isn't obvious from the numbers alone. It never is. To read what's actually happening you need two things — a framework for what these numbers mean, and enough history to know what they've meant before.

That's what this is.

What FCF and CAPEX actually tell you

Free cash flow is what a business generates after it's paid for everything it needs to keep running. Revenue minus operating costs minus the capital it spends maintaining and growing its physical infrastructure. It's the number Warren Buffett has called the closest thing to a company's true earnings — not the accounting profit, which can be shaped, but the actual cash the business produces.

Capital expenditures — CAPEX — is what a company spends building or buying long-term assets. Factories, servers, data centers, equipment. The things that don't show up as an expense this year but theoretically generate returns for years to come.

The relationship between the two is one of the most revealing signals in company analysis. A company generating strong FCF relative to its CAPEX is harvesting — running efficiently, returning capital, living within its means. A company running heavy CAPEX against thin FCF is betting — deploying today's resources against tomorrow's returns.

Neither is automatically right or wrong. The question is always the same: is the bet worth making, and can they survive long enough to find out?

History has a lot to say about both.

The companies that got it wrong

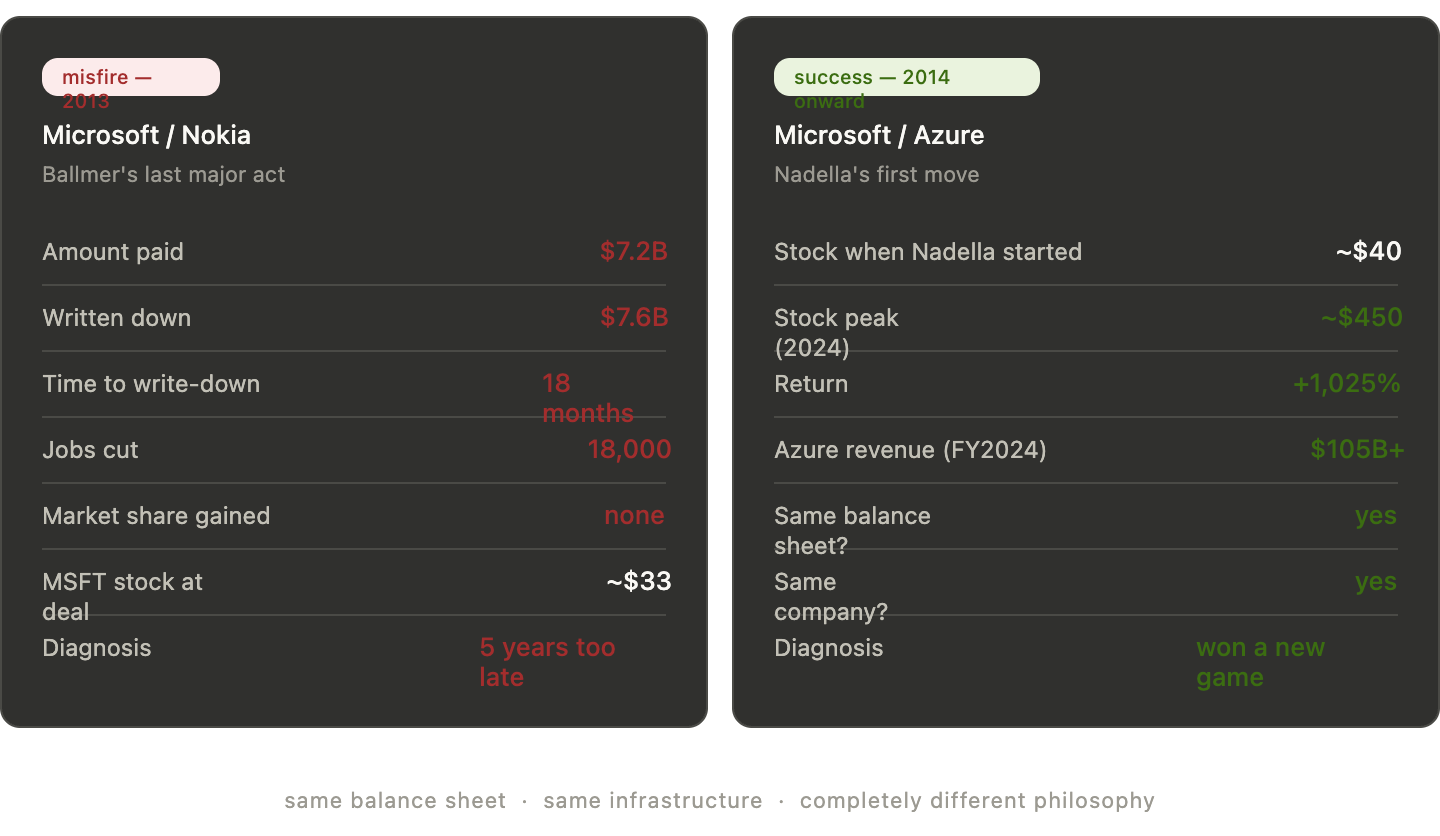

In 2013, Microsoft paid $7.2 billion for Nokia's handset business. At the time it was framed as a bold move into mobile — Microsoft planting a flag in the device market before it was too late.

It was already too late. Apple had released four generations of iPhone. Android had captured the low end of the global market. The consumer had decided, and Microsoft was trying to buy their way into a game the scoreboard had already settled. Within eighteen months they wrote down $7.6 billion — more than the entire purchase price — and laid off 18,000 people. The division was effectively shuttered.

The CAPEX wasn't wrong because mobile was a bad market. It was wrong because the deployment was reactive. They weren't building toward something — they were running from something. That distinction matters more than the dollar amount.

General Electric made a subtler version of the same mistake. Under Jeff Immelt, GE spent the better part of a decade and billions of dollars trying to reinvent itself as a software company. The initiative was called Predix — an industrial IoT platform that would sit on top of GE's physical infrastructure and generate recurring software revenue. The logic wasn't crazy. Industrial IoT is a real market.

The problem was organizational. GE was a jet engine company. A turbine company. A century-old industrial conglomerate whose competitive advantage lived in manufacturing precision and engineering depth. You cannot spend your way into a software culture. The technical talent didn't want to work there. The industrial customers didn't trust it. The product never found its market, and GE eventually sold or shut down most of it while the broader company fell apart around it.

The lesson from GE isn't that the idea was wrong. It's that CAPEX only works when it extends something a company genuinely has. You can build infrastructure. You cannot buy institutional DNA.

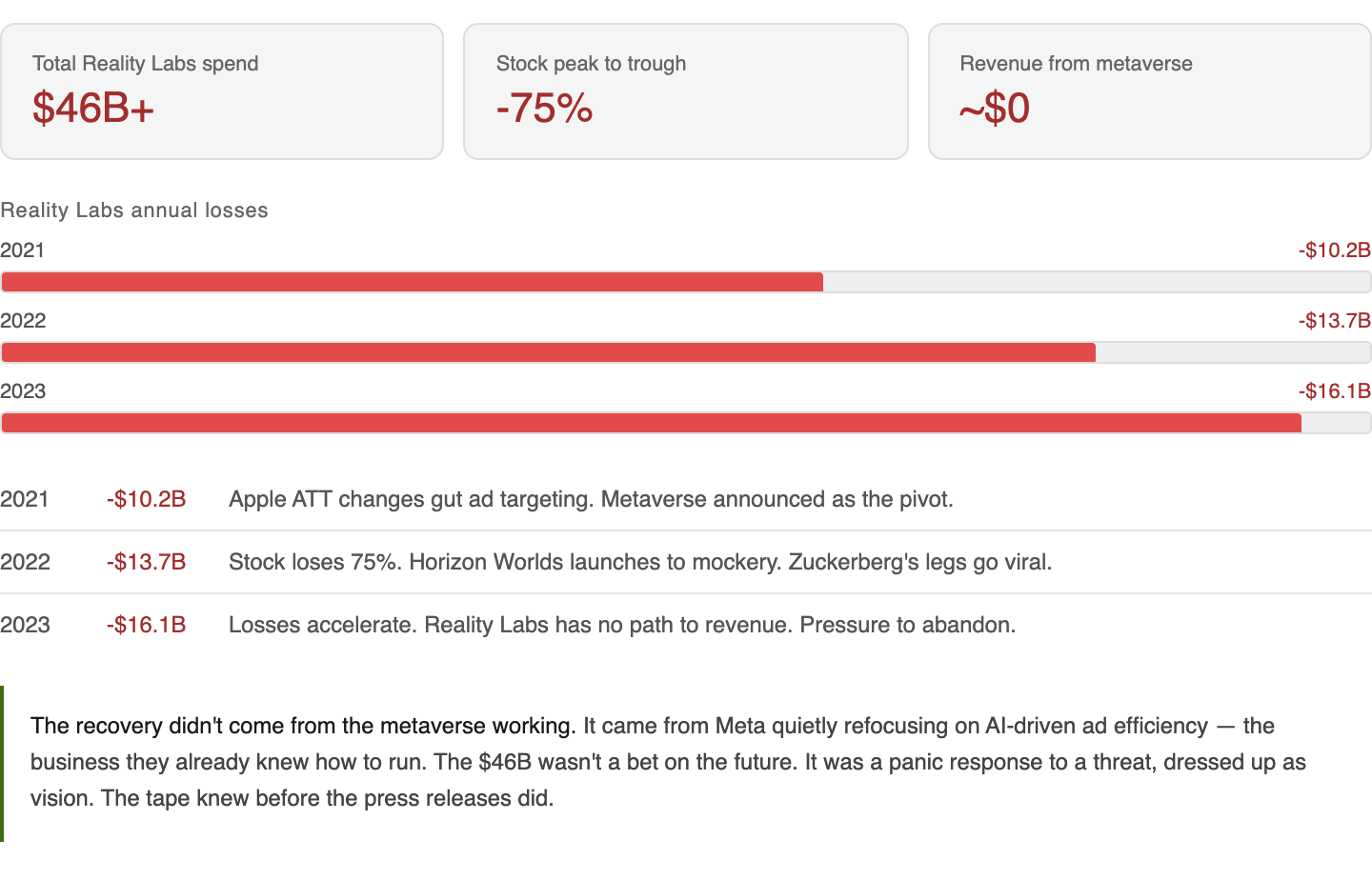

Meta learned a version of this the hard way. Between 2021 and 2023 they poured roughly $46 billion into Reality Labs — the metaverse division — chasing a vision of virtual social spaces that users never asked for and mostly didn't want. The honest read on that spending isn't that Zuckerberg lost his mind. It's that Apple's privacy changes had genuinely threatened Meta's core ad business, and the metaverse was a panic response that got dressed up as vision. The stock lost 75% of its value. The recovery came not from the metaverse working but from Meta quietly refocusing on AI-driven ad efficiency — the business they already knew how to run.

Panic capital is some of the most expensive capital in the world.

The companies that got it right

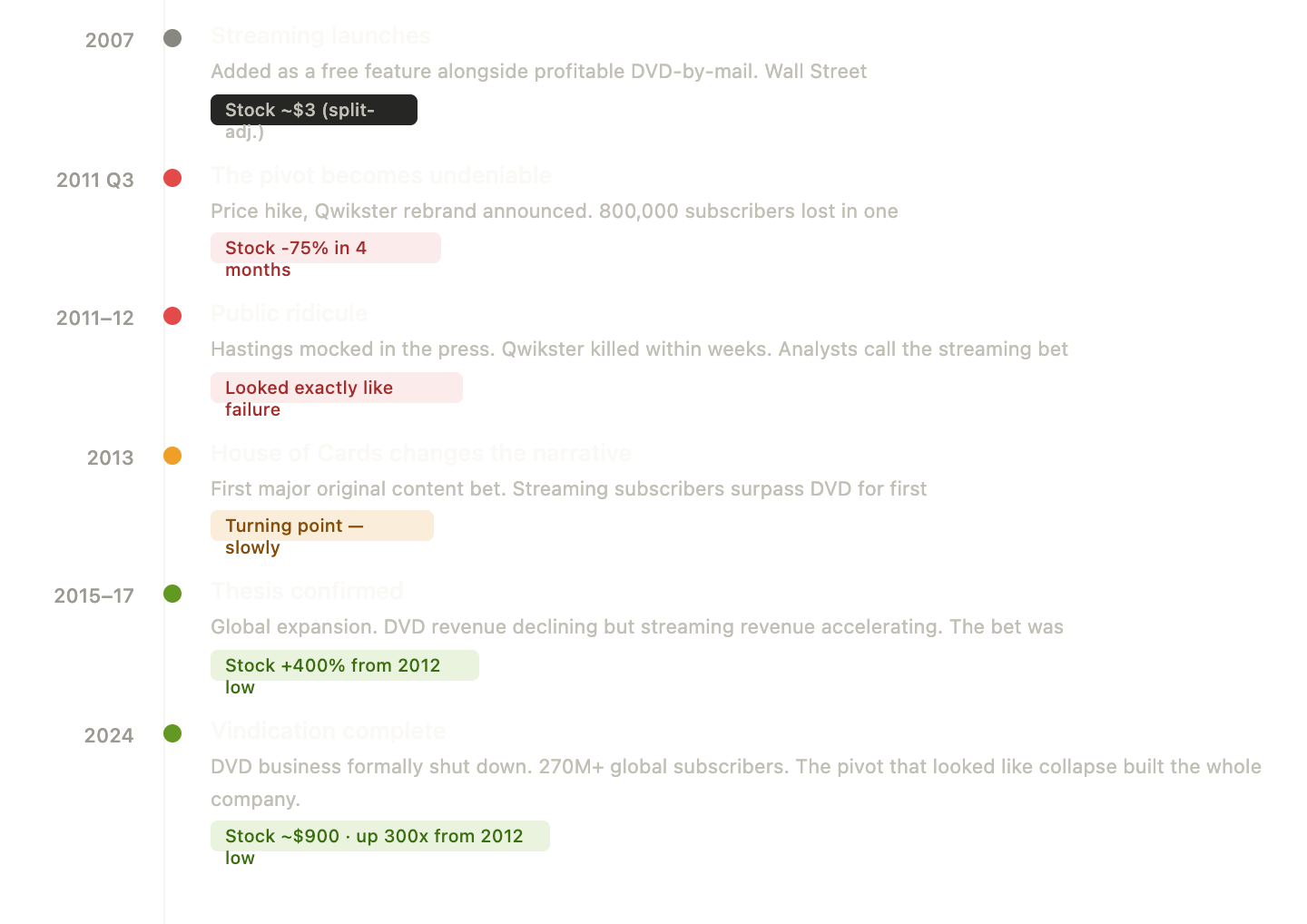

In 2007, Netflix was a DVD-by-mail company with a working business and a dangerous idea. Reed Hastings wanted to move everything to streaming — which meant voluntarily destroying the profitable physical business to fund infrastructure for a digital one that didn't yet exist at scale.

The stock dropped 75% in 2011 when the pivot became undeniable. Hastings was publicly ridiculed. The Qwikster rebrand — a fumbled attempt to separate the DVD and streaming businesses — became a cultural punchline. It looked, from the outside, exactly like a company making a catastrophic mistake.

What Hastings understood that the critics didn't was that broadband penetration had already reached the tipping point. Streaming wasn't a behavior Netflix was inventing — it was a behavior that already existed at the margins, waiting for infrastructure. The CAPEX wasn't creating demand. It was funding the infrastructure to meet demand that was already forming. That's a fundamentally different bet than building something and hoping people want it.

Amazon's AWS story has a similar shape but a more interesting origin. Jeff Bezos didn't sit down in 2003 and decide to build a cloud computing business. Amazon was scaling fast and their own engineers couldn't keep up — every team was rebuilding the same basic infrastructure from scratch. The solution was internal: build standardized, scalable computing infrastructure that any team could use. The product came second. They solved a real problem they actually had, then discovered that every other company had the same problem.

By the time AWS launched publicly in 2006 it looked like a strange side project from an online bookstore. For years it did. The retail business ran at razor-thin margins while AWS quietly compounded. Then AWS became the most profitable division in the company by a distance — 30%+ operating margins on a business that didn't exist before they built it. The years of looking unprofitable were years of building a moat that nobody could see yet.

Apple's story is different in a way that doesn't get enough credit. When Steve Jobs returned in 1997 Apple was weeks from bankruptcy. The reinvention that followed — iPod, iTunes, iPhone — was capital allocation as discipline rather than scale. Each bet was sequential. The iPod worked, so they funded iTunes. iTunes worked, so they funded iPhone. Each stage was funded by the previous stage's success, and each bet was concentrated rather than scattered. Jobs wasn't running ten moonshots simultaneously. He was running one at a time, making sure it worked, then moving.

That kind of discipline is almost impossible to replicate at scale. But it's worth understanding what it looks like, because it's the opposite of what most companies do when they feel threatened.

And then there is Microsoft — the most useful company in this entire conversation because they appear on both sides of the ledger.

The Nokia acquisition was Ballmer. Reactive, defensive, too late. The Azure buildout was Nadella. The same balance sheet, the same infrastructure, a completely different philosophy. When Nadella took over in 2014 the conventional wisdom was that Microsoft was a dying platform company — Windows losing relevance, mobile having passed them by, the stock flat for a decade. Instead of trying to recapture what they'd lost, Nadella invested in cloud infrastructure for a market that was just beginning to form. Azure wasn't built to defend Windows. It was built to win a game that hadn't started yet.

The stock was $40 when he took over. The rest is in the price.

Now look at the tape

Which brings us to right now. Because the seven companies currently being called the Magnificent Seven are running the largest synchronized capital expenditure experiment in corporate history. And the numbers are worth sitting with.

Apple and Nvidia are the outliers in opposite directions. Apple at roughly 10x FCF to CAPEX is harvesting — efficient, disciplined, not in the arms race in the same way. Whether that's wisdom or avoidance is a legitimate question. Nvidia is generating $83 billion in free cash flow against $19 billion in CAPEX not because they're being cautious but because they're the arms dealer. They're selling the infrastructure everyone else is buying. Their FCF dominance is a direct mirror of everyone else's spend.

Microsoft, Alphabet, and Meta are all spending more in CAPEX than they're generating in FCF. Amazon is the most extreme — $131 billion in CAPEX against $7.7 billion in FCF, funding the gap with operating cash flow and debt. Tesla is quiet by comparison, small absolute numbers on both sides, a company still figuring out what the next bet is.

The honest question this data raises is one history can't fully answer yet: is this the AWS moment or the Nokia moment? Is this Hastings killing the DVD business to fund the future, or is this Immelt spending billions trying to buy something that can't be purchased?

How long can they afford to be wrong

This is where the balance sheet becomes the final piece of the analysis. Because FCF and CAPEX tell you the rate of the bet. Cash on hand tells you the runway.

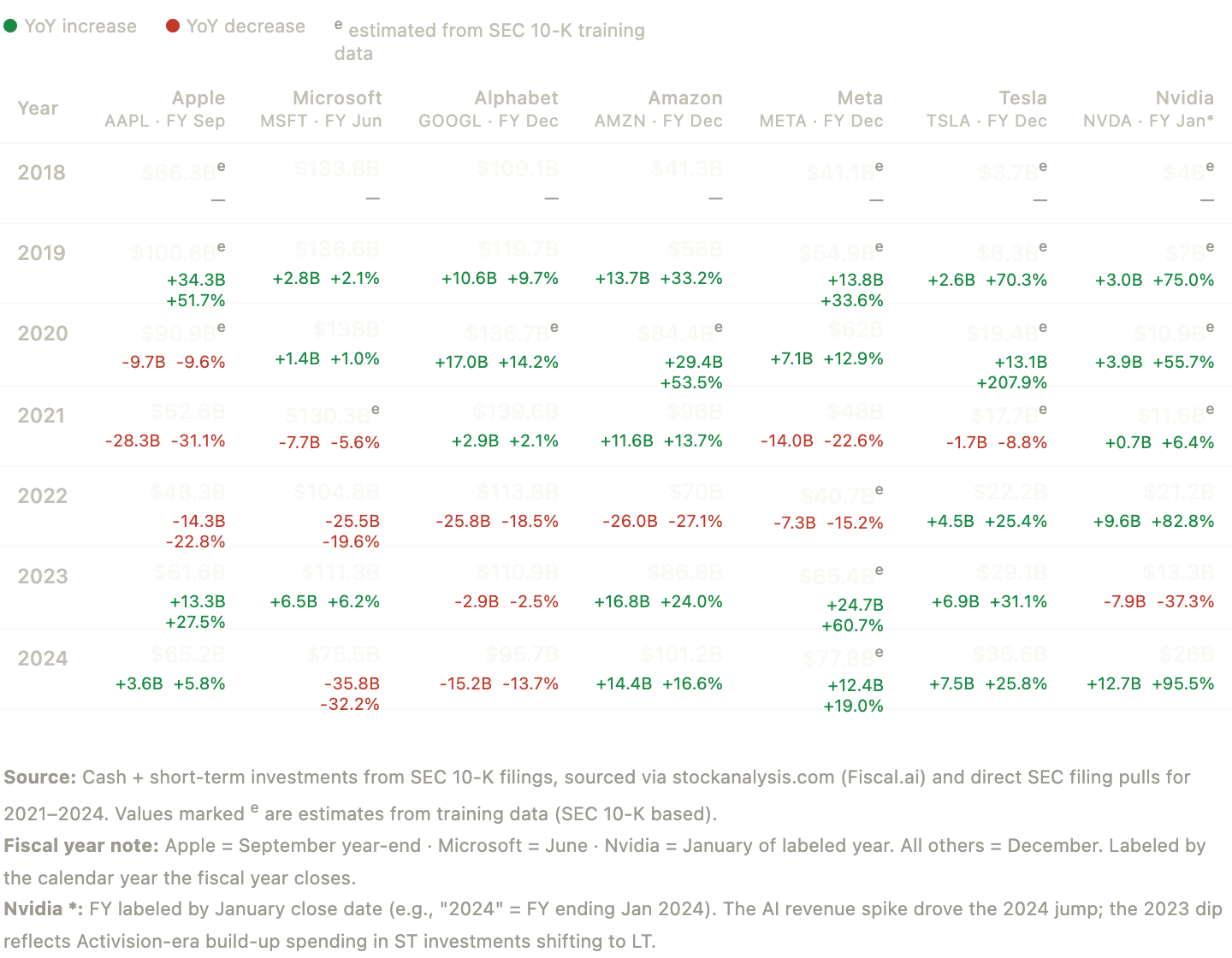

Microsoft sitting on $75 billion in reserves. Alphabet at $95 billion. Meta at $77 billion. These companies can sustain years of CAPEX-heavy operations without existential stress even if the AI infrastructure thesis takes longer than expected to generate returns. They've built the financial cushion to be wrong for a while and survive the learning period.

Amazon is the company to watch. The reserves are real but the rate of spend is unlike anything in their history. The parallel to the original AWS buildout is the one they're counting on. The parallel to Cisco's telecom bubble acquisitions — spending at scale on infrastructure just before demand plateaued — is the one nobody wants to say out loud.

The difference between those two outcomes won't be visible in the numbers for years. What the numbers can tell you right now is which companies are structurally positioned to find out.

That's what the tape is for.

A note on the data

FCF and CAPEX figures are trailing twelve months sourced from TradingView as of early 2026. Cash and short-term investments are annual figures from SEC 10-K filings sourced via stockanalysis.com. Fiscal year end dates vary by company — Apple closes in September, Microsoft in June, Nvidia in January, all others in December. Reality Labs loss figures are from Meta's annual 10-K filings. Netflix and Microsoft stock figures are split-adjusted historical prices.