Fees. How bad does 1% or less actually hurt in the long run?

A 1% annual fee sounds harmless — it's just a dollar per hundred. But because of how compounding works, that 1% charged every year doesn't just cost you 1% of your money. Over 30 years, it can cost you nearly a quarter of your entire portfolio. This post shows you exactly how that happens — and what to look for before you invest in anything.

Nobody tells you about fees when they're selling you something. They tell you about potential returns, historical performance, and the safety of having a professional manage your money. The fee is mentioned somewhere — it has to be, legally — but it's buried in a document, expressed as a small percentage, and presented as the reasonable cost of doing business.

It doesn't feel like much. Until you do the math.

The mechanics

Why a Small Percentage Is a Big Problem

Here's the thing about a 1% annual fee that most people don't intuitively grasp: it isn't charged on your original investment. It's charged on your total account value — every single year. And your account value grows over time, which means the fee grows too.

When your account is worth $10,000, a 1% fee costs you $100. When it's worth $100,000, the same 1% costs you $1,000. When it's worth $400,000 — the kind of balance a diligent saver might accumulate over a career — that 1% costs you $4,000 a year. Every year. Just in fees.

But the compounding problem goes deeper than that. Every dollar that leaves your account as a fee is a dollar that can no longer grow. It can't earn returns next year, or the year after, or for the rest of your investing lifetime. The fee doesn't just take money from you today — it takes away every future dollar that money would have become.

The numbers

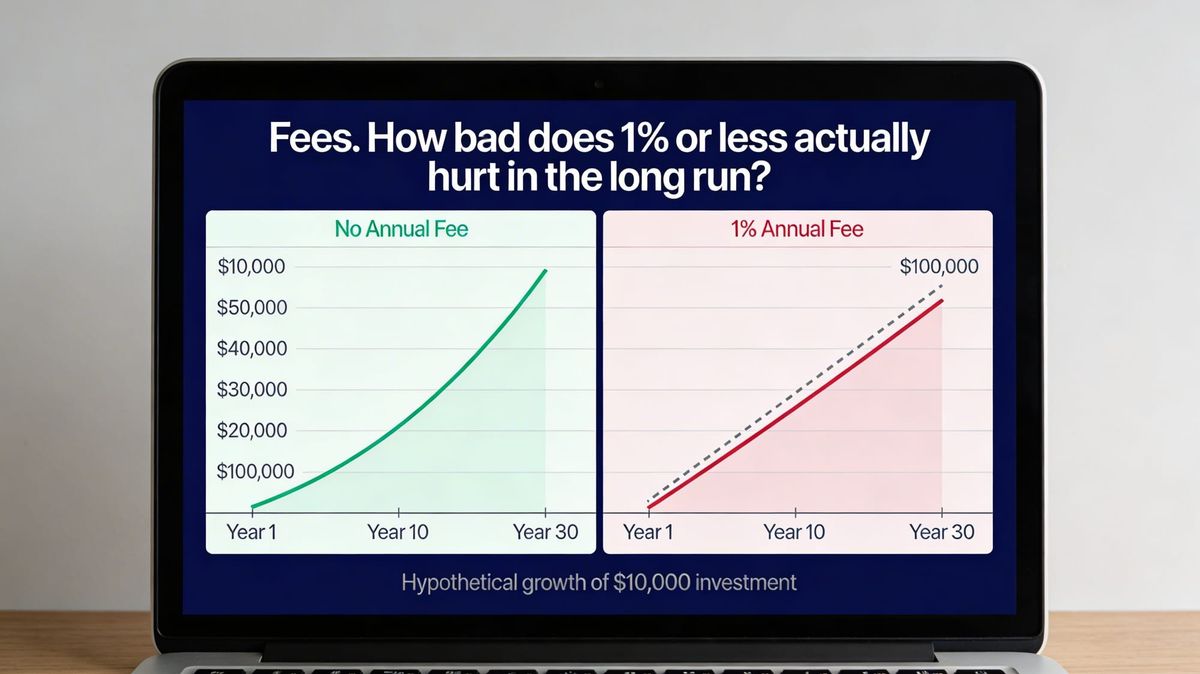

$10,000 — Three Paths, Three Very Different Outcomes

Let's make this concrete. Take $10,000 invested for 30 years, earning a 7% annual return before fees. The only thing that changes across these three scenarios is the annual fee.

Figure 1

$10,000 Invested Over 30 Years at 7% Gross Return

The only variable is the annual fee. All figures are hypothetical and illustrative.

The gap is striking. At a 0.03% fee — what you'd pay for a low-cost index ETF — your $10,000 grows to just under $76,000. At 1%, it grows to around $57,000. At 2%, it reaches only about $43,000. The 2% scenario leaves you with 43% less money than the 0.03% scenario — from the same $10,000 investment, the same market return, and the same 30 years. The only difference is the fee.

Figure 2

What Each Fee Level Actually Costs You After 30 Years

Compared to the lowest-fee option. The dollar amounts show what you lost to fees.

What to look for

How Fees Are Named — and Where to Find Them

The financial industry doesn't make this easy. Fees go by several different names depending on the product, and they're rarely presented in a way that makes their long-term impact obvious. Here's a quick reference for the most common ones you'll encounter.

Figure 3

Common Fee Types and What They Actually Mean

What each fee is called, where it shows up, and how to find it.

| Fee name | Where it appears | Typical range | How to find it |

|---|---|---|---|

| Expense ratio | ETFs, index funds, mutual funds | 0.03–0.5% | Fund prospectus or fund's webpage — always listed |

| Management fee | Actively managed funds, advisors | 0.5–1.5% | Account agreement or ADV form for advisors |

| M&E charge | Variable annuities | 1.0–1.4% | Annuity contract — often buried in the fine print |

| 12b-1 fee | Some mutual funds | 0.25–1% | Fund prospectus — covers marketing and distribution |

| Surrender charge | Annuities, some insurance products | 5–10% early | Contract terms — charged if you withdraw early |

The single most important number to find before investing in anything is the total annual cost — add up every recurring fee the product charges per year. For an index ETF, that's just the expense ratio. For a variable annuity or actively managed fund, you may need to add two or three separate charges together to get the real number.

The honest question

When Are Higher Fees Worth Paying?

Fees aren't automatically bad — they're bad when they're not justified by what you're getting in return. The question worth asking is: what am I paying for, and is it worth it?

A financial advisor who charges 1% per year might be worth every dollar if they're actively managing your tax situation, providing behavioral coaching that keeps you from panic-selling, and doing comprehensive financial planning. A mutual fund charging 1.5% might be worth it if it consistently outperforms its benchmark after fees — though the research on this is not encouraging. Most actively managed funds underperform their benchmark over long periods, after fees are accounted for.

The simplest rule of thumb: the higher the fee, the higher the burden of proof. Before paying more than 0.5% per year for any investment product, understand exactly what that fee is buying you — in plain language, not in marketing copy.

Low-cost index funds have democratized investing in a real way over the past 30 years. The ability to own a slice of 500 of the largest companies in the world for three cents per hundred dollars per year is genuinely remarkable — and it's available to anyone with a brokerage account.

You don't need to avoid all fees. You just need to know what you're paying, and why.